Key takeaways

- Unlisted shares are equity shares not listed on a recognised stock exchange; tax rules refer to them as "unquoted equity shares" for valuation purposes.

- Three regulatory frameworks govern unlisted share valuation: the Income Tax Act (Rule 11UA), the Companies Act (Sections 62, 42, Rule 13), and FEMA regulations.

- Rule 11UA prescribes the NAV (net asset value) formula for computing fair market value based on adjusted balance sheet figures; no external professional is required for NAV, but a SEBI-registered merchant banker is required to certify DCF valuations.

- The Companies Act requires valuations for corporate actions (preferential allotments, sweat equity, non-cash consideration, acquisitions/mergers, buybacks) to be conducted by an IBBI-registered valuer.

- FEMA regulations require that cross-border share transfers meet arm's-length pricing: at or above FMV when residents sell to non-residents, at or below FMV when non-residents sell to residents; pricing must be certified by a SEBI-registered merchant banker or CA with certificate of practice.

What valuation of unlisted shares means under Indian law

Unlisted shares are equity shares of a company that are not listed on any recognised stock exchange. Tax rules often refer to them as "unquoted equity shares," which include shares that are not regularly quoted on a recognised stock exchange.

Unlike listed shares, where the market price on a stock exchange provides an observable fair market value (FMV), unlisted shares have no publicly available price. The valuation must therefore be computed using prescribed methods.

Three distinct regulatory frameworks govern unlisted share valuation in India. Each law applies to specific types of transactions. Most founder transactions trigger only one law. Some trigger two. All three apply only in specific cross-border scenarios.

Rule 11UA of the Income Tax Act: Valuation of unquoted shares for tax purposes

Rule 11UA of the Income Tax Rules provides the mechanism for determining the FMV of unquoted equity shares for income tax purposes. It does not determine the transaction price but prescribes the FMV used for tax computation under the Income Tax Act.

During share transfers, this FMV may be used under provisions such as Section 50CA and Section 56(2)(x). If the agreed sale price is below the Rule 11UA FMV, Section 50CA may require the seller's capital gains to be calculated as though the shares had been sold at the FMV. Similarly, Section 56(2)(x) may tax the buyer on the difference between the FMV and the price paid if the statutory threshold (₹50,000) is exceeded.

How share valuation works under Rule 11UA

Rule 11UA lays down a balance-sheet formula (called the NAV method) that computes FMV based on adjusted book values of assets and liabilities. For the NAV method, no external valuation report is legally required; your accountant can compute it from audited financials. However, many transactions obtain a CA valuation report for documentation purposes.

For the DCF (Discounted Cash Flow) method, the valuation must be certified by a SEBI-registered Category I Merchant Banker. Chartered accountants could certify DCF valuations until a 2018 amendment to Rule 11UA restricted this role to merchant bankers.

Companies Act, 2013: Valuation requirements for share issuance and related transactions

When issuing shares in certain cases, the Companies Act, 2013 sets pricing and compliance requirements under provisions such as Sections 62 and 42. In these cases, valuation is used as part of the compliance process to determine or justify the issue price.

When is valuation required?

Valuation requirements typically arise under Sections 62 and 42 of the Companies Act, 2013, read with the Companies (Share Capital and Debentures) Rules, 2014, depending on the nature of the transaction.

Common scenarios include:

- Preferential allotment – When shares are issued to selected investors at a negotiated price, valuation is used to ensure compliance with prescribed pricing norms and justify the issue price.

- Sweat equity shares – When shares are issued to employees or founders for non-cash consideration such as services rendered, valuation helps determine the value of such contribution.

- Mergers and acquisitions – Valuation is used to determine share exchange or swap ratios between companies.

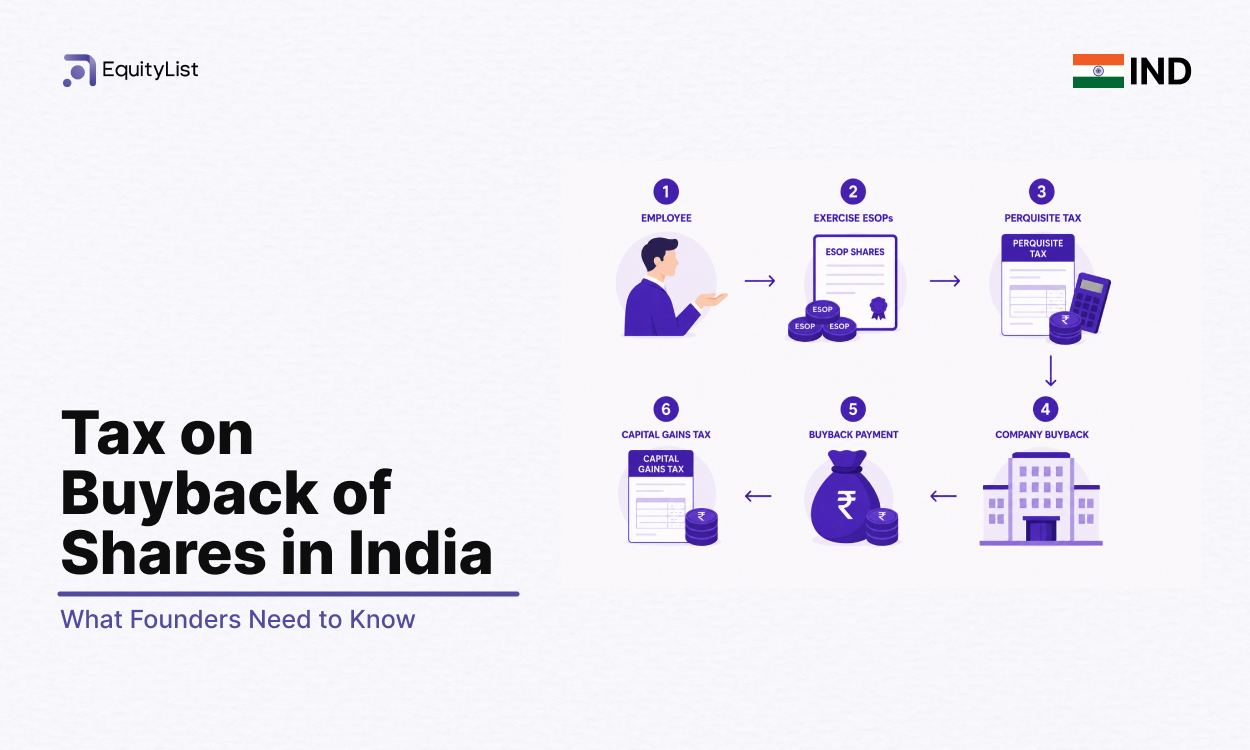

- Buybacks – Valuation may be used to support pricing decisions.

Who conducts the valuation

Where valuation is required under the Companies Act framework, it is generally carried out by a registered valuer, registered with the Insolvency and Bankruptcy Board of India (IBBI).

Registered valuers use recognised methodologies such as DCF, NAV, comparable company multiples, or other accepted approaches depending on the nature of the business and transaction.

FEMA: Valuation for cross-border issuance and transfers

When unlisted shares or other capital instruments are issued or transferred between a resident and a non-resident, pricing is governed by the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019.

- When a resident transfers or issues shares to a non-resident, the price cannot be lower than FMV.

- When a non-resident transfers shares to a resident, the price cannot be higher than FMV.

Thus, FMV acts as a regulatory floor or ceiling depending on the direction of the transaction.

FMV is generally determined using a valuation report issued by a SEBI-registered Category I merchant banker or a chartered accountant holding a valid certificate of practice.