Key takeaways

- Preference share valuation in Indian private companies is governed by three frameworks: income tax rules for issuance and transfer, FEMA for cross-border transactions, and the Companies Act for specific corporate actions.

- Angel tax under Section 56(2)(viib) was abolished effective FY 2025-26 and no longer applies to any issuance. Rule 11UA remains in force for open assessments from AY 2024-25 and earlier (covering fundraises up to March 2024), and as the reference framework for FEMA valuations.

- Rule 11UA prescribes NAV and DCF for issuances to resident investors. For CCPS specifically, Rule 11UA(2)(B) provides additional options: direct valuation via DCF, the VC fund price method, or the notified entity price method, or derivation from the underlying equity share FMV.

- DCF valuations under Rule 11UA require a SEBI-registered Category I Merchant Banker. CAs are no longer authorised for DCF certification under Rule 11UA but may still certify NAV-based valuations.

- For resident-to-resident transfers, Rule 11UAA applies. For equity shares, the NAV formula under sub-clause (b) is mandated. For preference shares, FMV is estimated as the open market price, with a merchant banker or accountant report. DCF is not available under either sub-clause.

- FEMA and NDI Rules require pricing at or above FMV for inward FDI and at or below FMV for outward transfers.

Preference shares in Indian private companies carry no market price. Their FMV must be computed under the regulatory framework that governs the specific transaction: income tax rules for issuances and transfers, Foreign Exchange Management Act, 1999 (FEMA) for cross-border transactions, or the Companies Act, 2013 for specific corporate actions. Which regime applies depends on the nature of the transaction and whether a non-resident is involved.

Issuing preference shares to resident investors

Rule 11UA of the Income-tax Rules, 1962 prescribes the methods for determining FMV when a private company issues preference shares to resident investors. Section 56(2)(viib) of Income Tax Act, 1961, the provision that once taxed issuances above FMV as income in the company's hands, was abolished by the Finance (No. 2) Act, 2024, effective FY 2025-26. For any issuance from April 1, 2025 onward, that provision no longer applies.

Rule 11UA itself remains in force. For companies with open assessments from AY 2024-25 or earlier, the rule governs those proceedings. The rule's valuation framework continues to apply for FEMA purposes on cross-border transactions. For any company with foreign investors, this is a continuing obligation.

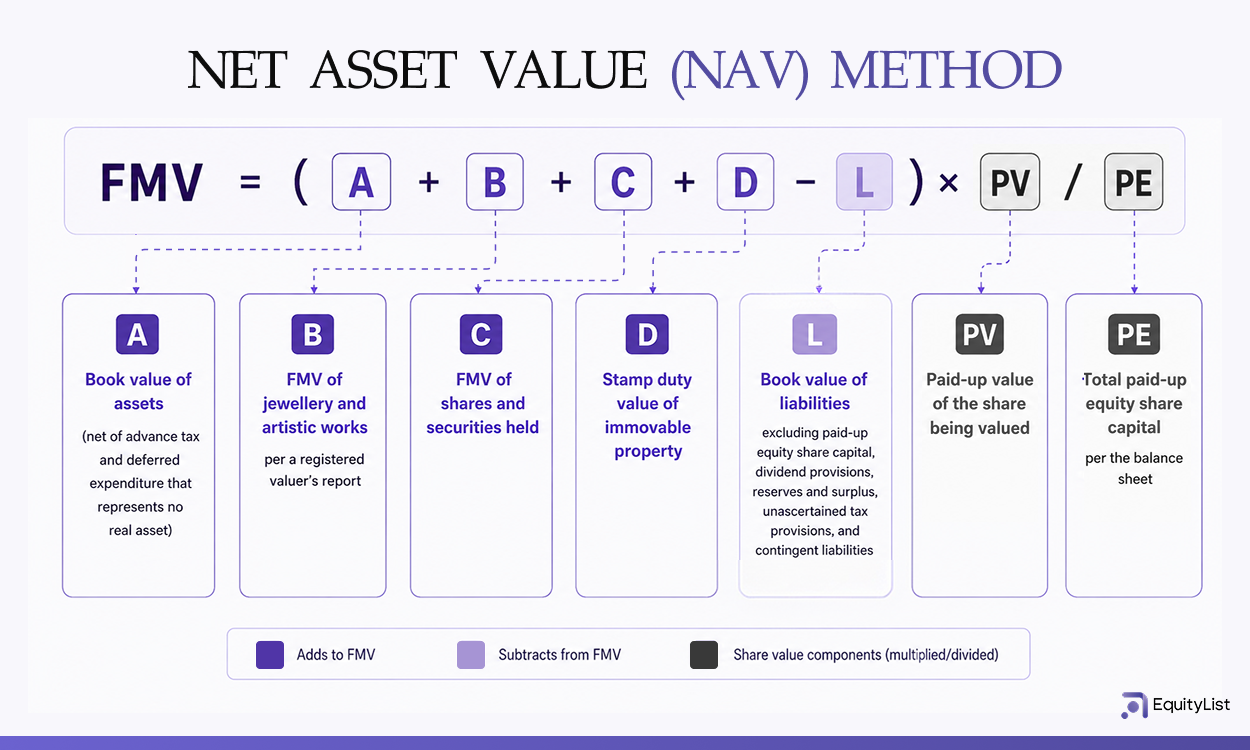

The Net Asset Value (NAV) method

The NAV method under Rule 11UA(1)(c)(b) derives FMV from the company's balance sheet using the formula:

FMV = (A + B + C + D − L) × PV / PE

The NAV method requires no projections, which makes it straightforward to apply and difficult to dispute. Its weakness is that it reflects historical book values. For a company where most value sits in future earnings rather than current assets, NAV may substantially understate economic value. For example, a company with ₹5 crore in net book assets but ₹500 crore in projected ARR will produce a very low NAV-based FMV regardless of what investors are willing to pay.

The Discounted Cash Flow (DCF) method

The DCF method requires a valuation by a SEBI-registered Category I Merchant Banker. Unlike NAV, which derives FMV from the company's current balance sheet, DCF derives FMV from the company's projected future earnings.

The merchant banker builds a model of future free cash flows, applies a discount rate that reflects the risk of those projections not materialising, and discounts the result to present value.

For growth-stage companies where most economic value sits in future earnings rather than current assets, DCF will typically produce a substantially higher FMV than NAV. The reliability of the output depends on the quality of the projections, and a DCF built on aggressive or unsupported assumptions carries the risk of challenge in an assessment or regulatory review.

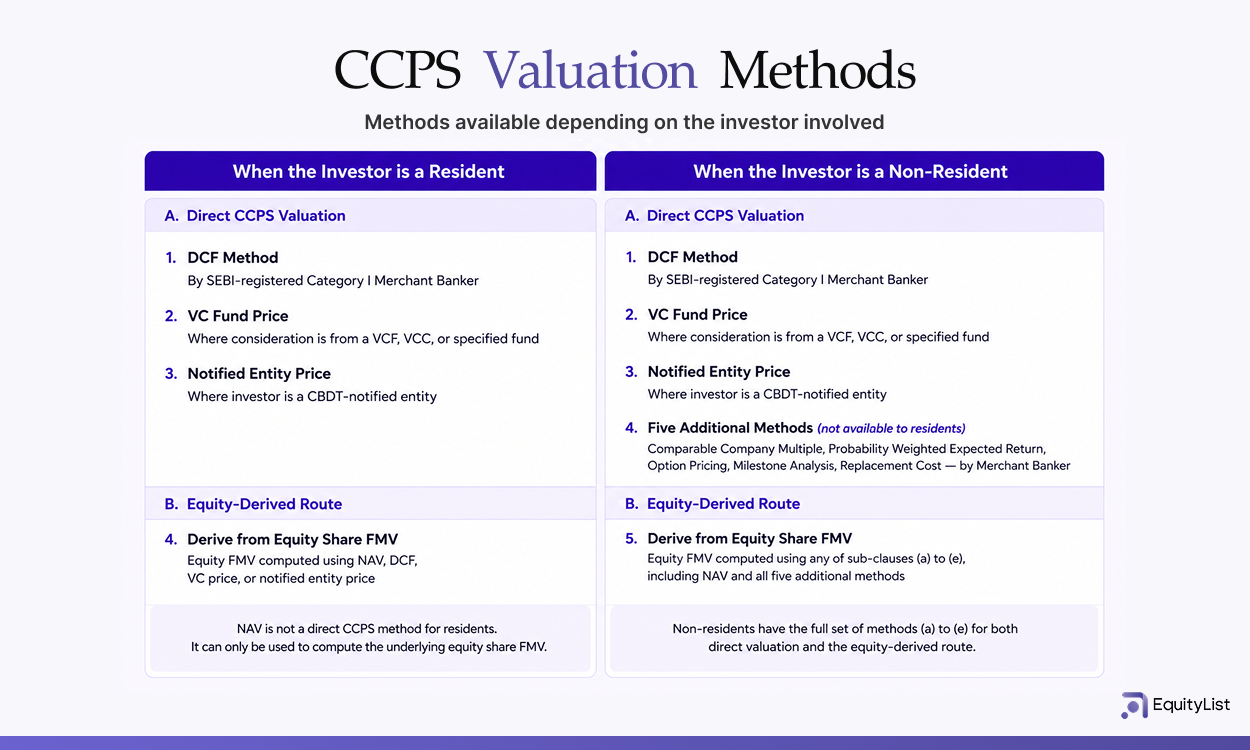

CCPS valuation under Rule 11UA(2)(B)

Before September 2023, Rule 11UA contained no explicit provision for CCPS. CBDT Notification No. 81/2023 introduced Rule 11UA(2)(B), which prescribes how to determine CCPS FMV directly.

For CCPS issued to resident investors, Rule 11UA(2)(B) gives the company two options.

- The first is to value the CCPS directly using DCF; the VC fund price method, where the conversion price is set at the price paid by an eligible venture capital fund in the same round; or the notified entity price method, where the price of the equity shares corresponding to consideration received from a notified entity within 90 days of the valuation date is taken as the equity share FMV, which is then used to derive the CCPS FMV.

- The second option is to derive CCPS FMV from the FMV of the underlying unquoted equity shares. For residents, that equity share FMV may be computed using NAV, DCF, the VC fund price method, or the notified entity price method.

For non-resident investors, sub-clause (d) of clause (A) makes five additional methods available, each to be applied by a SEBI-registered Category I Merchant Banker: the Comparable Company Multiple Method, the Probability Weighted Expected Return Method, the Option Pricing Method, the Milestone Analysis Method, and the Replacement Cost Method.

Transferring preference shares between residents

When preference shares change hands between two residents, both the seller and the buyer face separate tax consequences under the Income Tax Act.

Tax consequences for seller and buyer

Both provisions can apply to the same transaction. A below-FMV transfer simultaneously triggers a capital gains computation for the seller based on FMV and an income liability for the buyer on the shortfall.

How FMV is computed under Rule 11UAA

Rule 11UAA prescribes how to compute FMV for Section 50CA purposes when unquoted shares are transferred between residents. It cross-refers to Rule 11UA(1)(c) and is a separate rule from Rule 11UA, which governs issuances.

The applicable method depends on the type of share being transferred.

- For equity shares, Rule 11UAA mandates the NAV formula under sub-clause (b): (A + B + C + D - L) × PV/PE.

- For preference shares, sub-clause (c) applies. FMV is estimated as the price the shares would fetch in the open market on the valuation date. A merchant banker or accountant report may be obtained for this purpose.

DCF is not a prescribed method under either sub-clause. The valuation date is the date of transfer, not the balance sheet date.

Preference share transactions involving non-residents

When a non-resident subscribes to or transfers preference shares in an Indian private company, the transaction must comply with Rule 21 of the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019. The pricing requirement is directional.

This asymmetry is designed to discourage round-tripping (where money is sent abroad and returned as foreign investment to appear as FDI) on inward investment and capital flight on outward transfers.

Pricing rules under FEMA

Any internationally accepted methodology applied on an arm's-length basis is acceptable. The certifying professional must be a Chartered Accountant, a SEBI-registered Category I Merchant Banker, or a practising Cost Accountant in case of an unlisted Indian company.

Share swaps require a SEBI-registered Category I Merchant Banker or a recognised foreign Investment Banker. The certifier's registration details must appear on the face of the report.

Valuation reports are treated as valid for 90 days from the valuation date as per RBI Master Direction – Foreign Investment in India.

CCPS conversion price and the FEMA constraint

Under FEMA pricing rules, the conversion price at the time of conversion into equity must not fall below the FMV determined at the time of the original CCPS issuance. This constraint interacts with anti-dilution clauses: where a down round triggers a reset of the conversion price, and that reset price falls below the original FEMA floor, the conversion at the lower price may constitute a FEMA pricing violation. Companies and investors typically address this by restructuring the anti-dilution adjustment to preserve the FEMA floor, or by obtaining a fresh valuation at conversion to establish a new compliant FMV.

Valuation under the Companies Act

Certain corporate actions require valuation by an IBBI Registered Valuer in the Securities or Financial Assets category under Section 247 of the Companies Act, 2013.

This regime is separate from both the income tax and FEMA frameworks. A merchant banker or CA report prepared for Rule 11UA or FEMA purposes does not satisfy the Companies Act requirement where a registered valuer is mandated.

Who can certify the valuation of shares?

FAQs on preference share valuation

How are preference shares valued in Indian private companies?

Preference shares in Indian private companies have no market price, so FMV must be computed under the applicable regulatory framework. The governing framework depends on the transaction: issuances to residents fall under Rule 11UA of the Income-tax Rules, transfers between residents fall under Rule 11UAA, and any transaction involving a non-resident falls under FEMA. Each framework prescribes a different method and requires a different professional to certify the valuation. A merchant banker report, CA certificate, or IBBI Registered Valuer report may each be required depending on the context.

What is the valuation of preference shares for tax purposes?

For income tax purposes, FMV is determined under Rule 11UA (for issuances) or Rule 11UAA (for transfers). Rule 11UA offers two methods for resident investors: NAV, which uses the company's balance sheet, and DCF, which uses projected cash flows certified by a SEBI-registered Category I Merchant Banker. Rule 11UAA mandates the NAV formula for equity share transfers. For preference share transfers, FMV is estimated as the open market price with a merchant banker or accountant report. The FMV computed under these rules determines whether the seller faces a deemed capital gain under Section 50CA or the buyer faces an income adjustment under Section 56(2)(x).

What are the main valuation methods for preference shares?

In the Indian regulatory context, the primary methods are the Net Asset Value method, the Discounted Cash Flow method, and internationally accepted methods used for FEMA purposes such as earnings capitalisation and comparable transactions. NAV is mechanical and balance-sheet based. DCF is forward-looking and requires a SEBI-registered Category I Merchant Banker. For CCPS issued to non-resident investors, five additional methods are available under CBDT Notification No. 81/2023: the Comparable Company Multiple Method, the Probability Weighted Expected Return Method, the Option Pricing Method, the Milestone Analysis Method, and the Replacement Cost Method.