Many companies today are offering equity-based compensation through ESOPs, SARs, and RSUs. These instruments provide employees with a chance to benefit from the company’s growth.

But, understanding how these instruments work, especially in terms of taxation, can sometimes be a bit tricky.

So in this blog-post we’ll break down the taxation of these instruments in India.

What are ESOPs (Employee Stock Option Plans)?

ESOPs are a type of compensation offered by companies to their employees, granting them the option to purchase company shares at a predetermined price (known as the exercise or strike price).

ESOPs align employees’ interests with the company’s performance, as they directly benefit from the growth in the company’s share value.

How ESOPs work

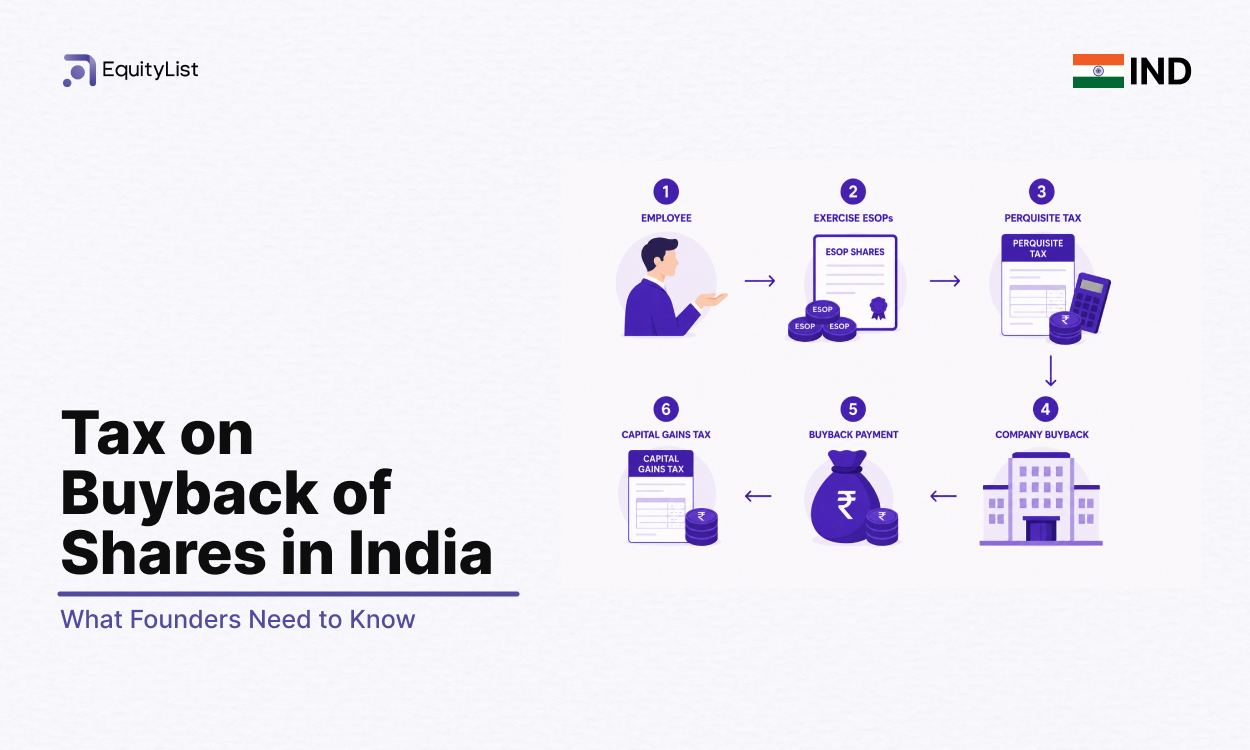

1. Grant

The company issues ESOPs grants to eligible employees as part of their compensation package.

It includes details like:

- Number of options granted.

- The exercise price (e.g., ₹100 per share).

- The vesting period and schedule (4 year vesting period with a 1year cliff, after which the options vest monthly).

The 1-year cliff means no options vest until 1 year, and after that, vesting can occur monthly, quarterly, or yearly, over the next 3 years depending on the company’s policy.

2. Vesting

Vesting refers to the period an employee must stay with the company to gain the right to exercise their options. Companies typically use a staggered vesting schedule.

Example:

If the vesting schedule is 25% annually over four years:

- Year 1: 250 options vest.

- Year 2: Another 250 options vest.

By the end of Year 4: All 1,000 options are vested.

3. Exercise

Once options are vested, the employee can purchase shares by paying the exercise price.

The difference between the exercise price and the current Fair Market Value (FMV) determines the profit.

Example:

FMV = ₹500

Exercise Price = ₹100

Profit per share = ₹500 - ₹100 = ₹400

Assuming the exercise happened after all 1000 options vested, your total profit would be (₹400 X 1000) = ₹4,00,000.

This ₹4,00,000 is now taxable income. Remember, this gain is not realised unless the employee sells the shares.

4. Sale

After exercising, the employee may choose to sell their shares to liquidate their profits. If the employee sells the shares at a higher price than what they bought it at, capital gains taxes may apply.

Capital gains tax is additional to the tax paid during exercise.

Example:

Sale Price = ₹700

FMV at Exercise = ₹500

Profit per share = ₹700 - ₹500 = ₹200

The total profit here if you sell all exercised shares would be (₹200 X 1000) = ₹2,00,000, which is liable for capital gains tax.

Taxability of ESOPs in India

Like we saw earlier, ESOPs are taxed at two stages:

a. Tax on exercise

The difference between FMV at the time of exercise and the exercise price is treated as perquisite income (a form of compensation) under the "Salaries" head and thus taxed accordingly.

Is TDS applicable on ESOPs?

Yes, the employer is responsible for deducting TDS on the perquisite value at the time of exercise and reporting it in your Form 16.

b. Tax on sale

When the shares are later sold, any gains are further taxed as capital gains. The tax depends on the holding period:

Short-Term Capital Gains (STCG)

If the shares are sold within 24 months (for unlisted shares) or within 12 months (listed) of exercise, the gains are treated as short-term capital gains and taxed at 20%, up from the previous rate of 15% as per the Budget 2024 announcement.

Long-Term Capital Gains (LTCG)

If the shares are held for more than 24 months (unlisted) or more than 12 months (listed) since exercise, the gains qualify as long-term capital gains and are taxed at 12.5%, up from 10%, following the Budget 2024 update.

This rate applies to gains that exceed ₹1.25 lakh, which is the threshold for long-term capital gains exemption applicable to all asset sales, including equity compensation.

Deferral of tax payment on ESOPs for eligible startups

The Finance Act, 2020 introduced a rule that allows employees of eligible start-ups, as defined under Section 80-IAC of the Income Tax Act, to defer paying taxes on the perquisite they receive when they exercise their ESOPs.

Here’s how it works

For eligible start-ups, tax deduction is not required immediately when employees exercise their ESOPs.

Instead, the tax payment is deferred until one of these events happens:

- 48 months (4 years) have passed since the end of the assessment year in which the shares were allotted to the employee.

- The employee sells the shares they received under the ESOP.

- The employee leaves the company (their employment ends).

Once one of these events occurs, the company must deduct the tax and pay it to the government within 14 days.

This reduces the upfront financial burden, especially when employees are unable to sell shares to pay taxes immediately.

What are Stock Appreciation Rights (SARs)?

SARs allow employees to benefit from the increase in the company’s share value over time, without actually owning the shares. Employees receive a payout equivalent to the appreciation in the share price from the date of grant to the date of exercise or settlement.

How do SARs work?

1. Grant

The company issues SARs to employees at a base value, which is typically the share price on the grant date.

2. Vesting

Similar to ESOPs, SARs vest over a specified period, and may include a cliff period.

After the cliff period, vesting typically occurs periodically, such as on a monthly, quarterly, or annual basis.

Employees can only claim the appreciation once the SARs have vested.

3. Settlement

Upon exercise of the vested SARs, the difference between the base value and the Fair Market Value (FMV) of the shares on the exercise date is paid to the employee either in cash or shares.

Example:

An employee is granted 1,000 SARs at a base value of ₹200 each. After four years, the SARs vest, and the FMV of the shares at the time of exercise is ₹500.

The appreciation per SAR = ₹500 (FMV at exercise) - ₹200 (Base value) = ₹300

Total payout = ₹400 × 1,000 = ₹4,00,000

The company can settle this ₹4,00,000 in cash or issue shares worth the equivalent value.

SARs taxation in India

If settled in cash

If the SARs are settled in cash, the payout is treated as salary income and taxed under the "Salaries" head.

The employer deducts TDS on this income and reports it in your Form 16.

Example:

- Grant price (Base price): ₹200 per SAR

- FMV at settlement: ₹500 per SAR

- Number of SARs: 1,000

Total appreciation:

The difference between the market price and grant price per share is: ₹500 - ₹200 = ₹300.

For 1,000 SARs, the total appreciation is ₹3,00,000.

The full amount of ₹3,00,000 is treated as taxable income and is taxed as perquisite income, similar to salary.

If settled in shares

In this case, the employee is taxed twice:

The first time, when they receive the equivalent value of the shares, which in this case is ₹3,00,000 worth of shares. This as well is treated as salary income and taxed accordingly.

The second time is when the employee eventually sells these shares. At this stage, capital gains tax applies to the difference between the sale price and the FMV at the time of settlement.

What is an RSU (Restricted Stock Unit)?

RSUs (Restricted Stock Units) give employees the right to receive shares of the company stock after meeting certain conditions like vesting or performance goals.

Unlike stock options, RSUs are not dependent on the employee purchasing the shares but automatically vest into shares when they meet the conditions.

Taxation of RSUs in India

Like ESOPs, RSUs are also taxed in two stages: at vesting and at sale.

a. Tax implications on vesting

When RSUs vest, they are treated as perquisite income. The taxable amount is based on the Fair Market Value (FMV) of the shares on the vesting date.

Example:

- Number of RSUs: 250

- FMV of the shares: ₹500

- Taxable Amount = ₹500 × 250 shares = ₹1,25,000

This ₹1,25,000 will be added to the employee's salary income and taxed accordingly. Employees don’t receive ₹1,25,000 in cash but rather 250 stocks worth ₹500 each.

b. Tax implication at sale

When the employee sells the shares, capital gains tax applies to the difference between the sale price and the FMV at the time of vesting.

If the employee sells the shares for ₹600 per share (after they vest at ₹500), the capital gain is ₹600 - ₹500 = ₹100 per share.

If 250 shares are sold, the capital gain will be ₹100 × 250 = ₹25,000.

Depending on the holding period of the shares, STCG or LTCG will apply.

Is U.S. RSU taxable in India?

Yes, If an Indian resident holds RSUs granted by a US-based company, the RSUs are taxed in India at the time of vesting and sale. At the time of vesting, employees need to pay tax in the year of vesting or within two and a half months of the end of the year in which vesting occurred.

If you are a non-resident of the US, you aren't subjected to US Federal tax.

Any deductions you see are likely from a ‘sell-to-cover transaction’, where the employer sells a portion of your shares to cover the Indian TDS liability.

However, if taxes were paid in the U.S., the employee can claim a foreign tax credit for those taxes when filing their Indian tax return, thanks to the Double Tax Avoidance Agreement (DTAA) between India and the U.S.

We hope you found this blog-post helpful. In case you have any questions, reach out to us here.